Renting vs. Buying: The Numbers Might Surprise You

Renting vs. Buying: The Numbers Might Surprise You

Renting often feels like the simpler path. There’s no large down payment to save, no responsibility for a broken furnace, and no long-term mortgage commitment tying you down. On the surface, it offers flexibility and fewer upfront expenses.

But then the lease renewal arrives — and the rent increases. Again. Over time, those steady hikes can turn “flexible” into financially draining. Meanwhile, each monthly payment builds your landlord’s equity, not yours. It’s easy to feel stuck in a cycle where you’re paying more without gaining ownership.

There’s also constant conversation about housing affordability. Headlines frequently suggest buying a home is out of reach. Yet when you look beyond the noise and actually compare numbers, the reality may surprise you.

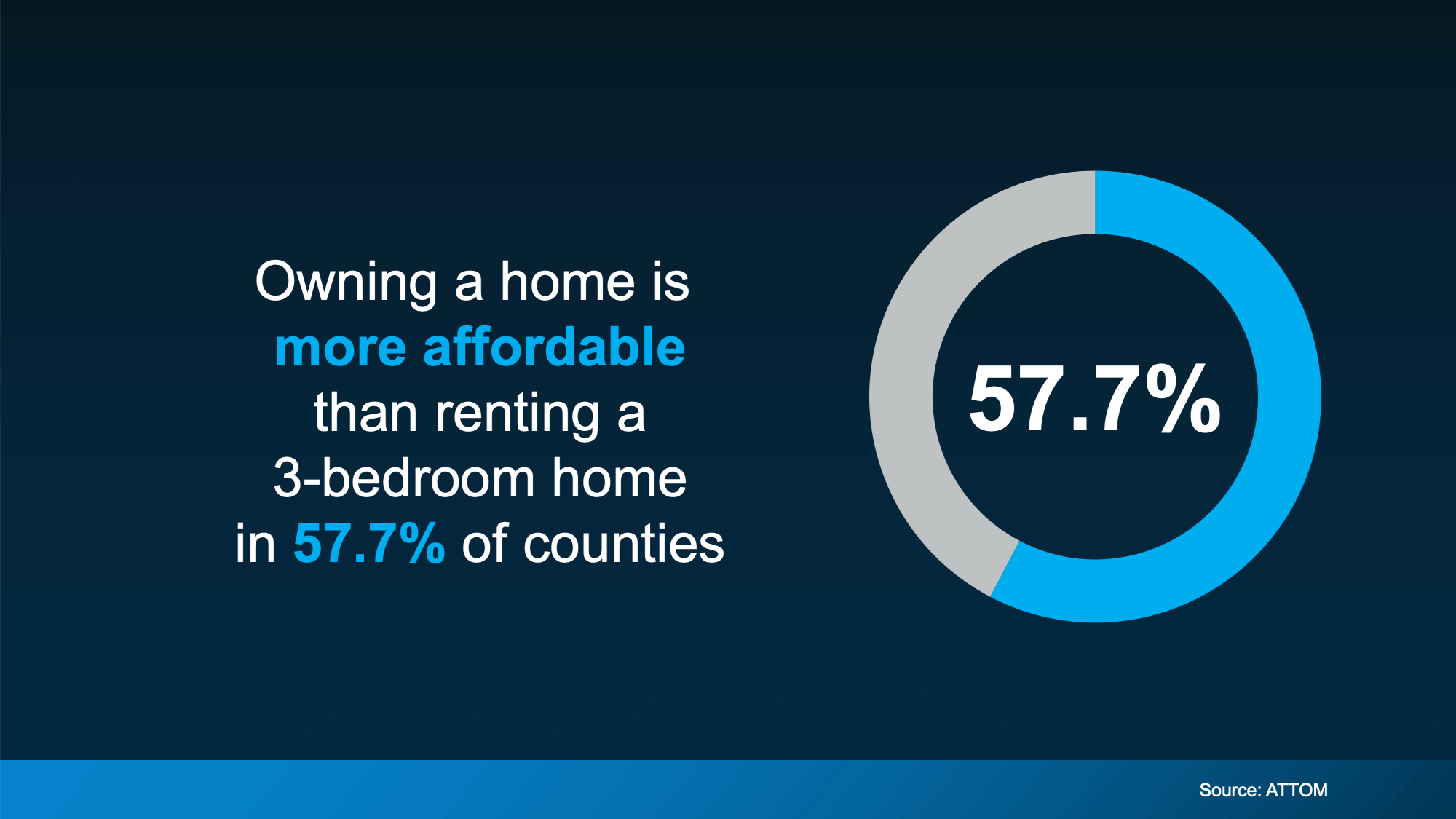

Homeownership vs. Renting: The Monthly Cost Comparison

In many markets today, owning a home can cost less per month than renting a comparable three-bedroom property. When factoring in principal, interest, property taxes, insurance, and even estimated maintenance, the total monthly cost of ownership is often competitive — and sometimes lower — than rent.

Why is this happening?

-

Home price growth has moderated in many areas

-

Housing inventory has improved in certain markets

-

Mortgage rates have stabilized compared to recent peaks

At the same time, rents have continued climbing in numerous cities, placing increasing pressure on monthly budgets.

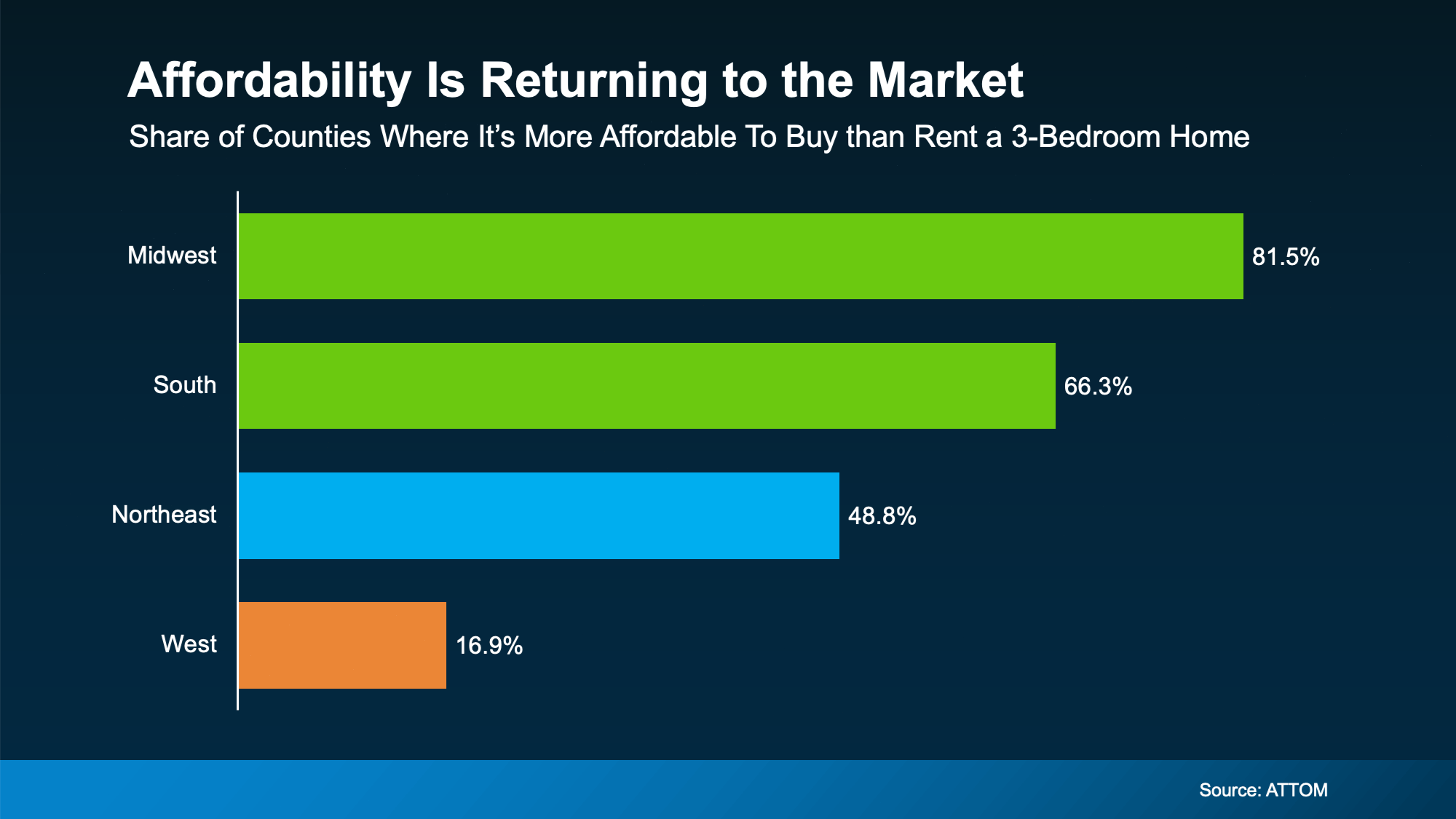

Location Matters

Of course, real estate is local. Housing affordability varies significantly depending on where you live. In parts of the Midwest and South, buying has become increasingly attractive compared to renting. In some Western markets, affordability remains more challenging.

The key takeaway: national averages don’t tell your personal story. A local market analysis is the only way to truly determine whether buying makes financial sense in your area.

The Real Barrier: Upfront Costs

For many renters, the biggest obstacle isn’t the projected monthly mortgage payment — it’s the down payment and closing costs.

Here’s what often gets overlooked: thousands of down payment assistance programs exist nationwide. Many buyers qualify without realizing it. Assistance can sometimes cover a meaningful portion of upfront costs, significantly lowering the amount needed to purchase a home.

When you combine potential assistance programs with competitive monthly payments, homeownership may be more achievable than it initially appears.

The Bigger Picture

This isn’t about rushing into a purchase. It’s about understanding your options. Renting isn’t automatically the cheaper or safer financial choice. In some markets, buying may offer more stability, predictable payments, and long-term wealth building.

If you’re currently renting and wondering whether ownership could work for you, a simple review of the numbers can provide clarity. Sometimes the biggest step isn’t moving — it’s just starting the conversation.

Recent Posts

GET MORE INFORMATION